A collections agent picks up an inbound call on a Monday morning. The caller identifies herself by full name, confirms identity details, and asks to discuss settlement options on a Capital One account, requesting both the lump sum offer and the monthly payment plan. She confirms details, requests a reference ID for a portal account, thanks the agent, and hangs up.

The entire call lasts about seven minutes. It's polite, organized, and completely unremarkable, except for one thing: the caller isn't a person. It's an AI agent, calling on behalf of the borrower.

What we're seeing

Across multiple collection agencies we work with, we've seen thousands of these calls over the past few months. All from AI agents acting on borrower's behalf. Most calls run over five minutes.

The bot is collecting information, building a complete picture of what's on the table, so whoever deployed it can make a decision offline.

And it's working. The calls go through without friction because the bots aren't doing anything suspicious. They're cooperative, patient, well-spoken. They pass verification. They follow the flow an agent expects. Nothing about the interaction triggers a red flag.

How we actually spotted them

A customer success team reviewing call data at one of our partner agencies noticed a cluster of inbound calls that all followed the same sequence. The structure was almost identical every time, with the caller using nearly the same words to confirm identity, ask for "both a lump sum and a monthly payment option," and close with phrases like "I'd like to take some time to think about these options." This unnatural consistency across dozens of calls was the first major flag.

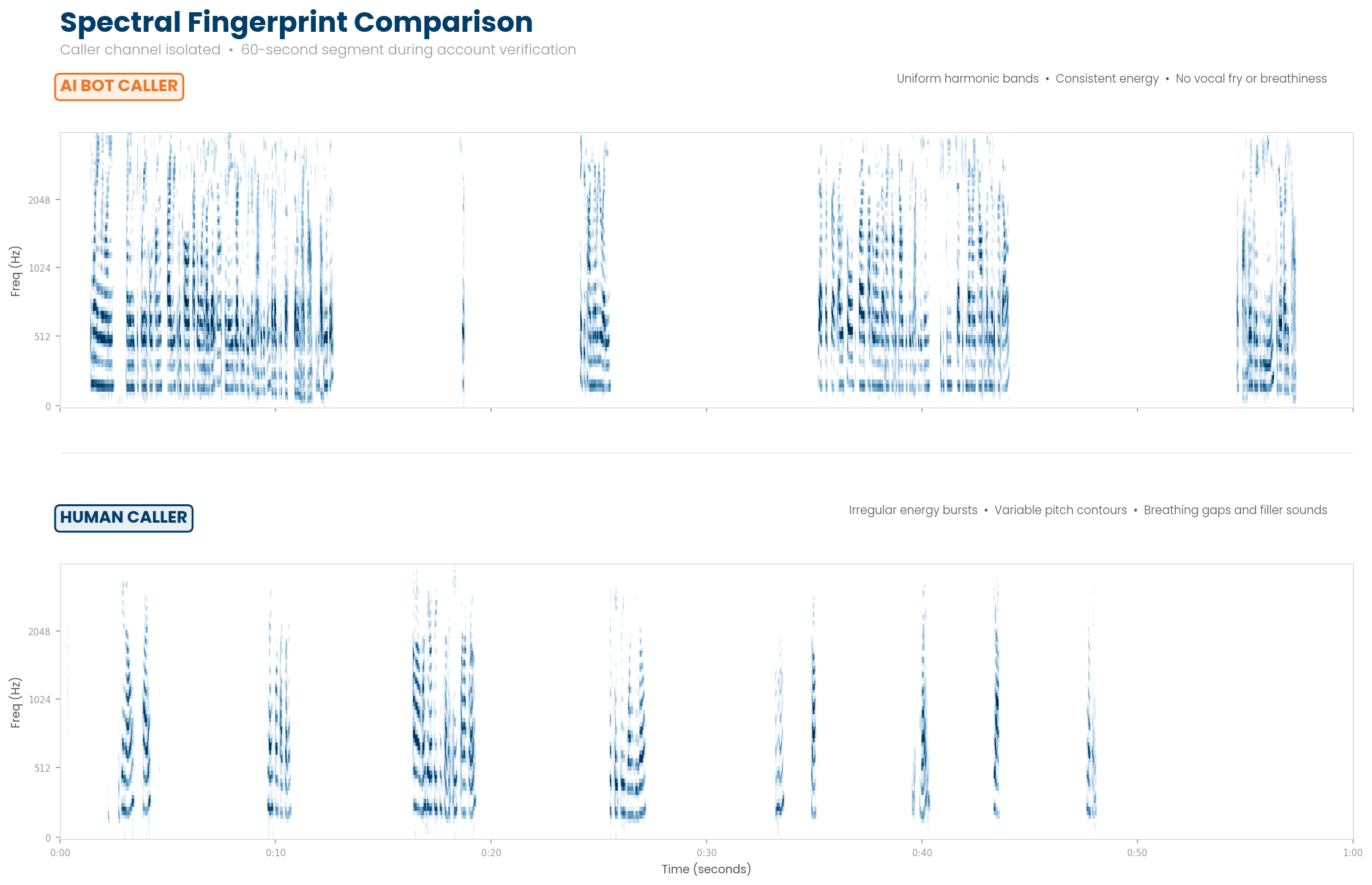

This is what a voice looks like when you break it down into its frequency components. The bot caller's voice produces clean, repeating patterns every time it speaks — almost like a machine printing the same shape over and over. The human caller's voice is rougher, less predictable, with energy showing up in different places each time. That messiness is normal. It's what human speech looks like. The uniformity in the bot's voice is the tell.

This tracks how the caller's voice rises and falls in pitch over the course of the conversation. The bot stays almost flat — same pitch, same rhythm, utterance after utterance. The human jumps around. Their voice goes up when they ask a question, drops when they trail off, spikes when they're making a point. That variation is how people naturally talk. The bot sounds natural enough in the moment, but over 60 seconds the flatness becomes visible.

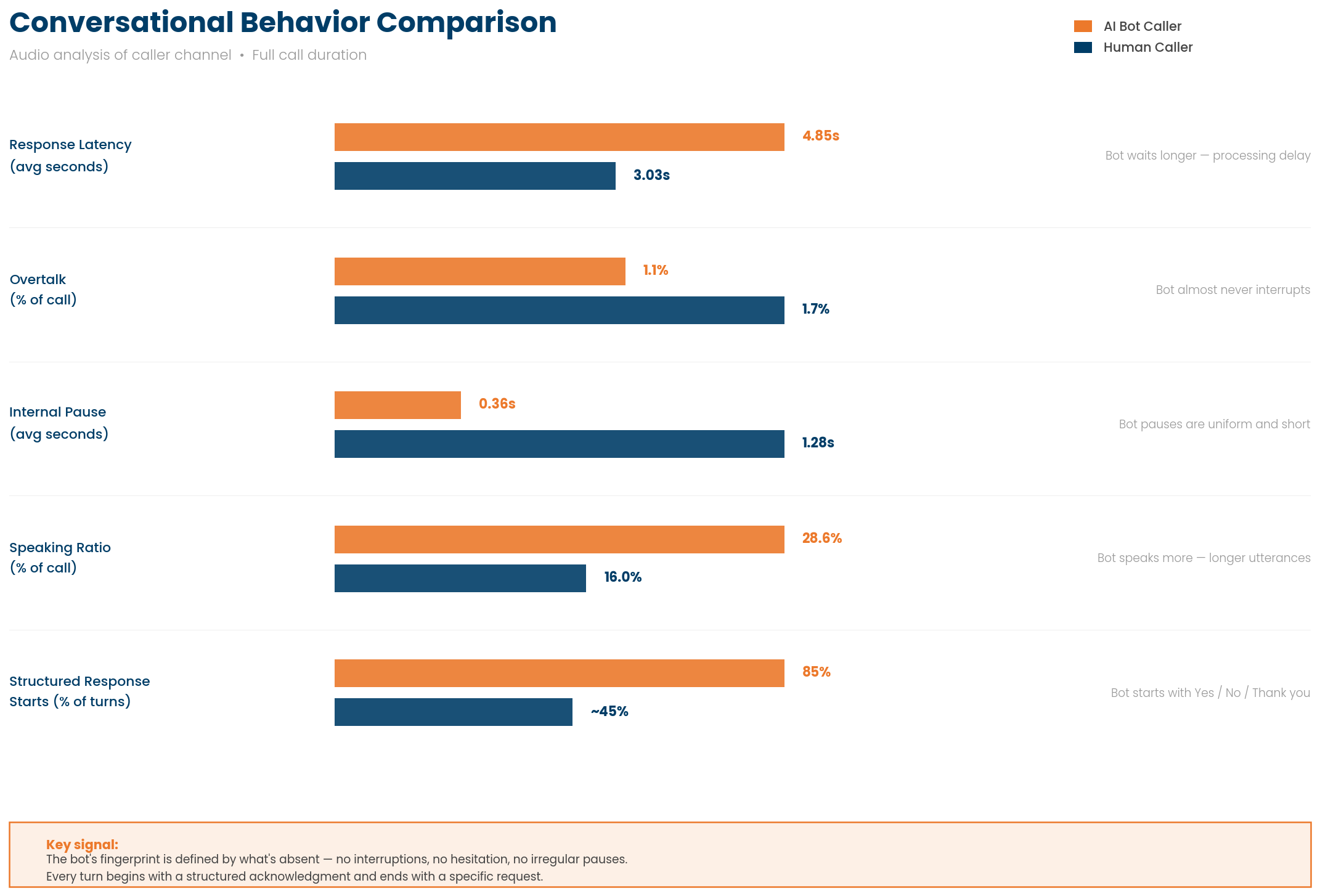

Five patterns that separate a bot from a borrower. The bot waits longer before responding, almost never talks over the agent, pauses for a fraction of the time a human would between sentences, talks for a larger share of the call, and starts nearly every response with "Yes," "Thank you," or "That's correct." Any one of these on its own means nothing. All five together, consistently, across hundreds of calls — that's a fingerprint.

Why this is difficult to catch

For the agent on the other end, there's no obvious signal. If you're handling 40 calls a day and most of them follow a similar pattern, you're not going to stop and wonder whether the pleasant, cooperative caller on the line might be a machine.

There are open questions about whether standard verification protocols hold up when the entity on the other end is software rather than a person, but that's a legal conversation still developing. The more immediate operational question is simpler: how do you even know it's happening?

What's actually shifting here

Collections has spent the last several years building AI into its own operations.

These bot calls flip that assumption. Borrowers, or the fintech services they're hiring, now have access to the same underlying technology.

That changes the negotiation dynamics in a real way. Collections has historically operated with an information advantage. The servicer knows the account history, the available offers, the expiration timelines, and the borrower's likelihood to pay. A bot that methodically extracts every data point the agent is willing to share starts to close that gap.

And the current generation of these bots is conservative. They're gathering information, not pushing back. They don't counter-offer, dispute nor escalate. But there's nothing technically stopping the next version from doing all of that.

How we think about this at Prodigal

We first noticed these calls through proInsight, which monitors 100% of interactions across our customers' operations.

Detection came first. We built a "Bot caller" tag that identifies these interactions based on behavioral signatures: conversational formality, structured request sequences, absence of emotional cues, and consistent information-gathering without commitment.

Detection alone doesn't solve anything. The more useful question is what agents should do differently. Today they handle bot calls the same way as every other inbound call — full verification, full disclosure, full offer presentation. Through proAssist, we can surface a different playbook when bot indicators are detected: a different escalation path, different disclosure protocols, or a supervisor flag before sharing offer details. The tooling already exists; the specifics depend on what each servicer decides is appropriate.

The most interesting layer is aggregate intelligence. If we can identify which accounts bot callers are targeting and track whether those accounts convert through proPay afterward, we start to understand the actual impact — whether bot calls are a leading indicator of payment, or part of a pattern where borrowers are mapping their options across every debt before deciding where to put their money. That turns a novel phenomenon into operational intelligence.

Where this goes

The thousands of bot calls we've tracked across our customers are an early signal, not an isolated event. Consumer-facing AI tools are getting cheaper and easier to deploy. The barrier to a borrower using an AI agent to handle their debt calls is dropping fast, and once a service proves it can get borrowers better outcomes, adoption will follow.

Collections operations that start instrumenting it now, detecting it, measuring it, understanding the conversion patterns behind it, will have a clearer picture of what's happening in their portfolios and better options for how to respond.

The industry spent years figuring out how to deploy AI into its own operations. Now it needs to figure out what to do when AI shows up on the other end of the line.

Disclaimer: Analysis based on two real calls — one identified as an AI bot caller, one from a human borrower — with the caller's voice isolated from each recording.

.webp)

.jpg)

.jpg)

.png)

.webp)

.jpg)

.jpg)

.jpg)

.webp)

.webp)

.webp)

-min.avif)

.avif)

-modified.avif)

.avif)