Understanding Purchase Price Multiples (PPM) in debt collections and why they’re not enough anymore

In the debt collections world, Purchase Price Multiple (PPM) is often used as a simple but powerful metric to evaluate the return on investment (ROI) from acquiring a portfolio of delinquent accounts. But while it's a starting point, looking at PPM in isolation can be misleading, especially with the rising delinquencies, litigation risk, and operational costs of today.

In this blog, we uncover:

What PPM really means?

What a “good” multiple looks like?

How to adjust PPM to reflect real profitability?

What investors and operators should do next?

What is a Purchase Price Multiple (PPM)?

PPM = Total net collections / Original purchase price of the portfolio

For example:

You buy a portfolio for $10M Over time, you collect $22M Therefore, your PPM = 2.2x

A 2.0x PPM means you’ve collected twice the amount you paid for the portfolio. It’s the industry’s shorthand for profitability, underwriting success, and operational strength.

What PPM doesn’t show you?

A PPM is gross, not net of operating costs. It does not account for:

That’s a meaningful difference, especially for investors, CFOs, and strategists who are forecasting recovery margins.

What should PPM ideally be?

Most portfolios aim for >1.8x PPM

After costs, a Net PPM of ~1.4x–1.8x is considered moderately successful

Below 1.3x Net PPM, portfolios often underperform after factoring in risk and time

The more automation, segmentation, and smart workflows you apply, the closer your Net PPM stays to your Gross PPM. That’s the key to long-term scalability.

{{cta-banner}}

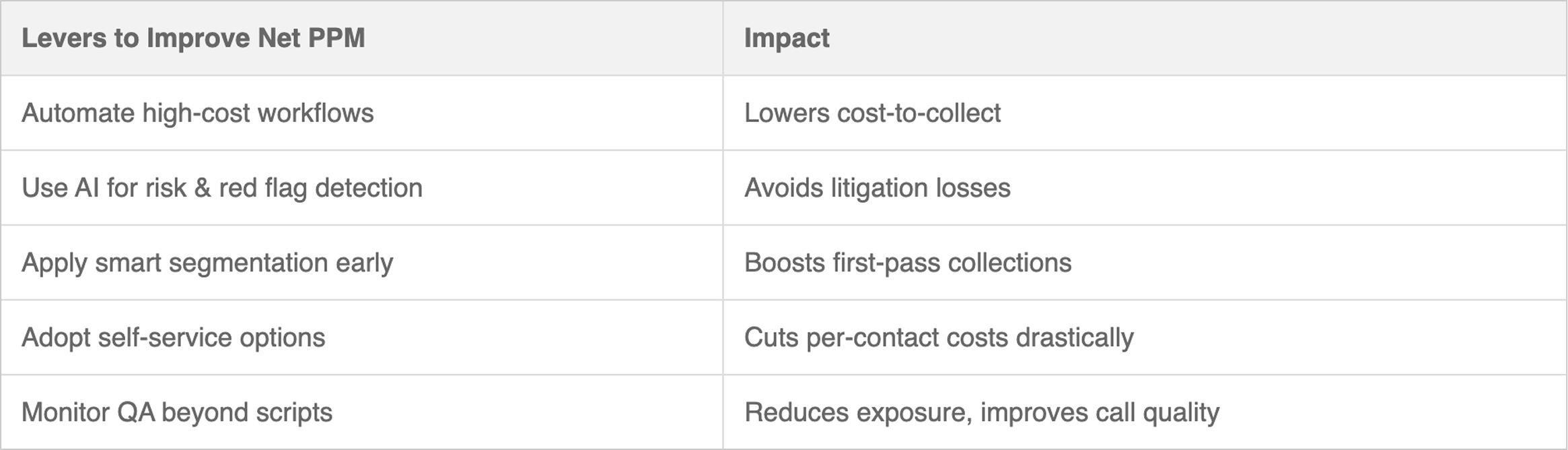

So what can debt buyers do?

Conclusion: From vanity metric to real indicator

PPM is a useful metric, but not a sufficient one.

To truly measure portfolio performance, investors and operators must:

Compare actual vs. estimated PPMs over time

Adjust for cost-to-collect and compliance risks

Prioritize systems that lower cost while protecting consumer experience

In a space where margins are tightening and complexity is rising, the smartest organizations are asking not just “what’s the multiple”, but “what’s the real return after the cost of doing it right?”

{{cta-banner}}

Collections

Operations

Business strategy

Know what’s dragging down your returns.

ProInsight helps uncover compliance gaps and operational blind spots before they erode your margins.

.webp)

.jpg)

.jpg)

.jpg)

.webp)

.webp)

.webp)

-min.avif)

.avif)

-modified.avif)

.avif)

.avif)

.avif)