Debt collection can be complex, especially when legal time limits come into play. At the center of this challenge is the statute of limitations, the legally defined period during which a creditor or collector can take legal action to recover unpaid debts. This window typically ranges from 3-6 years, depending on both the type of debt and the state’s laws.

The statute of limitations is more than a compliance requirement. It shapes how and when collection efforts can occur. Staying within these limits protects organizations from legal exposure while ensuring collection practices remain ethical and effective. At the same time, knowing when a debt becomes time-barred is crucial for adjusting strategies and maintaining consumer trust.

In this article, we’ll walk through the types of debt and their statutes of limitations, review state-specific differences, outline how to handle time-barred debts and explain how these rules affect credit reports.

What is the statute of limitations on debt collection?

The debt statute of limitations is the legally defined period during which a creditor or debt collector can file a lawsuit to recover unpaid debts. This timeframe differs based on the type of debt, the state laws where the debtor lives, and the contract terms.

Once this period expires, the debt is considered "time-barred," meaning creditors can no longer take legal action to enforce repayment. However, they may still try to collect the debt through informal methods.

The statute of limitations on debt collection is the legally defined period during which a creditor or debt collector can file a lawsuit to recover unpaid debts. This period varies depending on three factors:

- Type of debt (credit card, medical, auto, personal loan, etc.)

- State laws where the debtor resides

- Contract terms tied to the obligation

Once this period ends, the debt becomes time-barred. Creditors cannot sue to enforce repayment, but they may still attempt to collect through other means, such as calls, letters, or settlement offers.

Why does the debt statute of limitations exist?

The statute of limitations isn’t just a legal technicality, it exists to balance fairness between creditors and consumers. It ensures timely action while protecting individuals from the indefinite threat of lawsuits.

Here’s why these laws matter:

- Protection against old claims: Prevents consumers from facing lawsuits on decades-old debts, offering closure and legal certainty.

- Encouraging timely action: Pushes creditors to pursue claims promptly, reducing risks of lost evidence or records.

- Fairness in legal proceedings: Ensures both parties have access to accurate documentation, keeping disputes balanced.

- Supporting financial stability: Helps individuals recover financially by limiting the long-term burden of old debts, enabling greater economic participation.

What types of debt are there and their statutes of limitations in the US?

The statute of limitations on debt isn’t the same for every obligation. Different types of debt fall under distinct state laws, often shaped by the kind of contract behind them. For example, the limitation period for a credit card account may not match that of a personal loan or a verbal agreement without written terms.

These classifications determine how long creditors have the legal right to sue for repayment. For both lenders and consumers, understanding these distinctions is critical to navigating debt-related disputes and compliance obligations.

What is the statute of limitations on debt by the US states?

The statute of limitations on debt is not uniform across the country. Each state sets its own rules and timeframes, which can vary not only by jurisdiction but also by the type of debt. For creditors, agencies, and servicers, understanding these differences is essential to designing collection strategies that remain legally compliant.

Your state of residence plays a major role in determining how long a creditor has to file a lawsuit. A written loan contract in one state may allow six years for legal action, while another state may only allow three. The same is true for credit cards, oral agreements, and promissory notes, all of which may carry distinct timelines.

What are best practices for collectors handling time-barred debt?

When a debt becomes time-barred, collectors can no longer sue to enforce repayment because the statute of limitations has expired. At this stage, how collectors handle the account is just as important as whether they pursue it at all. Mishandling time-barred debt risks violating consumer protection laws and damaging trust.

Although collection agencies may still request voluntary repayment, strict compliance with laws like the Fair Debt Collection Practices Act (FDCPA) is essential. Any misrepresentation such as implying that legal action is still possible, can trigger lawsuits or regulatory penalties.

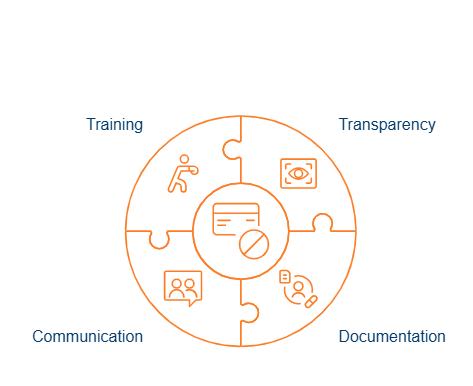

Here are best practices for approaching time-barred debt:

- Transparency: Clearly disclose when a debt is time-barred and explain the consumer’s rights regarding repayment.

- Documentation: Maintain detailed records to confirm whether the statute of limitations has expired, avoiding disputes over debt validity.

- Communication: Maintain detailed records to confirm whether the statute of limitations has expired, avoiding disputes over debt validity.

- Training: Equip collection teams with up-to-date knowledge of federal and state laws to ensure ethical handling of older debts.

Conclusion

The statute of limitations sets clear boundaries for lawful debt collection, defining when legal action is possible and when a debt becomes time-barred.

Strong practices like keeping accurate records, training agents on state-specific rules, and using compliant communication help minimize risk and promote ethical recovery.

Many organizations now rely on AI agents like proAgent, which manage consumer conversations across voice and digital channels while embedding compliance into every interaction.

With this support, collections teams can handle even sensitive cases effectively, ensuring recovery strategies remain legal, consistent and consumer-first.

FAQs (Frequently Asked Questions)

1. How long until a debt is no longer valid?

The law does not erase the debt but limits the period when a creditor or collector can take legal action to collect it. This time frame varies by state but ranges from 3 to 6 years.

2. What happens after 7 years of not paying debt?

Typically, most debts are removed from the debtor's credit report after seven years. However, certain types of debt, such as tax liens or unpaid medical collections, may remain for up to 10 years or potentially longer. Paid medical debt collections and other derogatory marks may not always appear on the debtor's credit report.

3. What is the final proof of debt?

The final proof of debt letter outlines the total amount a creditor is entitled to claim when a debtor enters an insolvency process, serving as the official record of the debt owed.

%201.png)